Summary (for the time poor)

Part 1 of the guide explores how leveraging property—using borrowed money to buy real estate—can significantly accelerate wealth creation compared to investing the same amount in shares.

Leverage allows investors to control more valuable assets with less of their own money, meaning returns are generated on the full value of the property rather than just the initial investment.

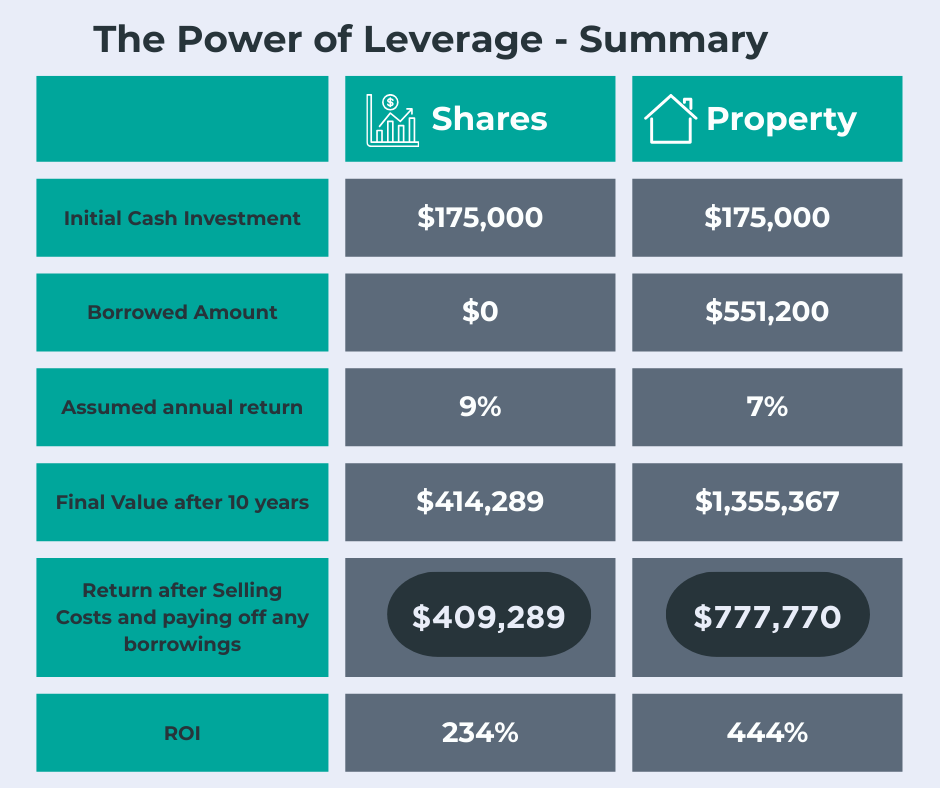

For example, with $175,000, an investor could either buy shares outright or use that amount as a 20% deposit on a $689,000 property. Even using an assumed annual return for shares being higher (9%) versus 7% for property, the larger asset base enabled by property leverage leads to significantly greater returns over the years.

Using these figures as an example, a property investor could achieve an ROI of 444% with leveraged property compared to 234% with shares (over a 10 year period - see below for more details).

Borrowing to invest in shares, typically through Margin Loans, is also considered very high risk due to the potential for margin calls and forced sales during market downturns. In contrast, as long as mortgage repayments are maintained, property investors won't be forced by a lender to sell even in a declining market.

The guide emphasizes that while property investing has its own risks—such as market fluctuations and the burden of debt—careful planning, selecting good locations, and focusing on cash flow can mitigate these issues.

Overall, the use of leverage in property, when managed responsibly, can be a powerful strategy for building wealth and achieving long-term financial goals. This is demonstrated in the summary table below for our example scenario (explained further below).

(In Part 2 of this guide, we will cover how you can leverage equity in existing property to continue to leverage and build your portfolio and wealth.)

Understanding Real Estate Leverage

In the realm of wealth creation, understanding the power of leverage can be the difference between plodding along and achieving your life dreams.

Using leverage in property investing allows investors to amplify their purchasing power, enabling them to acquire higher valued assets (and more properties) and potentially increase their returns.

By exploring the importance of leverage in property investment, and comparing this to investing in shares, Part 1 of this guide aims to equip you with an understanding of the basics of leverage and contrasts possible returns in leveraged property versus shares.

Importance of Leverage

Leverage in property investing is a game-changer, allowing investors to control larger assets with a smaller initial investment. This financial strategy can significantly boost returns and accelerate wealth creation.

By using borrowed capital (i.e. Other People’s Money or OPM), investors can purchase properties that might otherwise be out of reach. This increased purchasing power opens up opportunities for diversification and portfolio growth.

Leveraged Property Investing Basics

Leveraged property investing involves using borrowed funds to purchase real estate. The basic principle is to use a small amount of your own money and borrow the rest from a lender.

Here's a simple breakdown of how it works for your first investment property:

- Use your own money to cover the deposit and buying costs (typically 20-25% of the property value)

- Secure a mortgage for the remaining amount

- Use rental income to cover mortgage payments and expenses, and

- Benefit from property appreciation over time.

The power of leverage lies in its ability to generate returns on the TOTAL VALUE of the property, not just your initial investment. This can lead to substantial wealth creation over time.

Leverage and Share Investing

It is possible to use leverage to invest in Shares but this is widely regarded as very high risk.

According to https://moneysmart.gov.au/how-to-invest/borrowing-to-invest, borrowing to invest in shares is done by using what is called a Margin Loan.

Under this type of loan, if you share value drops too much (noting too that shares are very volatile) you get a margin call.

If so, you generally then have 24 hours to address this margin call, where you can:

- Deposit more money to reduce your margin loan balance, or

- Add more shares or managed funds to increase your portfolio value (for this you of course need more funds), or

- Sell part of your portfolio and pay off part of your loan balance.

If you can't address the margin call, your margin lender may sell some of your investments.

Noting the above and how volatile the share market is, you can see that you could easily be forced to desposit more money or be forced to sell when you don’t want to.

Borrowing for Property does not carry this massive risk; as long as you can keep paying the interest repayments a bank will not force you to sell or produce more money.

Investing your Money in Shares versus Leveraged Property

The best way to demonstrate the power of leverage is to look at an example.

Let’s assume you have $175,000 in cash you want to invest. You are considering:

- Investing this in Shares

- Investing this in your first investment Property together with borrowings (i.e. using leverage).

Disclaimer – it should be noted that the following example and details are reasonably simplistic in nature and do not account for personal situations, tax rebates, the entity or entities owning the asset or additional contributions (to shares or onto the mortgage).

Let’s first consider your upfront costs

The upfront investment costs for this example are assumed to be as follows.

Investing in Shares

- Cash injection $175,000

- Assuming no buy costs or major initial fees

Investing in Property

When buying property there are more upfront costs as compared to Shares. For this example these are assumed to be:

- Stamp Duty $24,000

- Solicitor/conveyancer $2,500

- Pest and Building inspection $700

- Buyer’s Agent $10,000

- TOTAL BUYING COSTS = $37,200

It is important to note that these buying costs can all be added to your Cost Base which helps to reduce your Capital Gains Tax obligation when/if you decide to sell.

This means:

- $37,200 from your available cash of $175,000 = $137,800 left over.

- You use the $137,800 as your 20% deposit for the property.

- This means you can afford a property valued at $689,000.

- Leaving you with borrowings required of $551,200.

In summary:

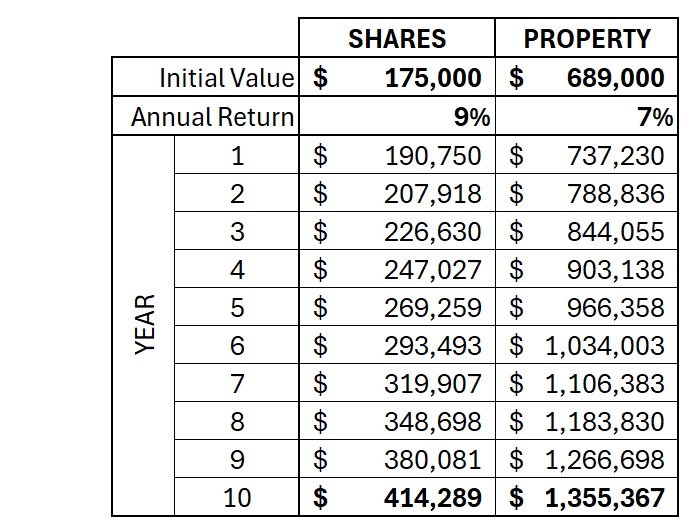

- With Shares your initial asset value will be $175,000

- With leveraged Property your initial asset value will be $689,000

Gains over 10 years – the raw power of Leverage

There is a lot of available data regarding past performance of shares and property. According to savings.com.au, property tends to out-perform (Australian) shares when you consider rental income and tax offset – refer to this article for more information https://www.savings.com.au/home-loans/property-vs-shares.

However, for this example, we will assume the following annual returns in our calculations.

- Shares 9%

- Property 7%

Based on these annual estimated returns, the following table shows the compounded value of your investment over 10 years.

This table demonstrates the huge power of leverage! Even with a smaller annual return, the fact that the return is based on a higher valued asset/amount shows the dramatic impact leverage (and compounding) has.

Leveraged Property produces a significantly higher gain

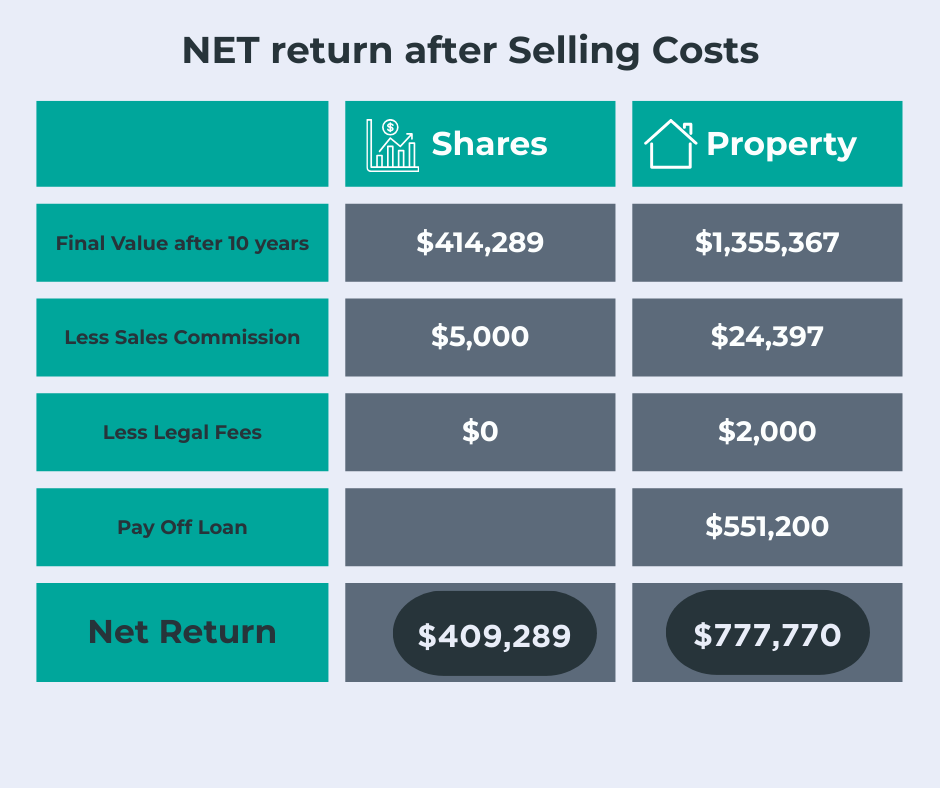

Whilst not every investor sells after 10 years, it is only fair to demonstrate the NET return of the 2 scenarios after selling costs and paying off the property loan.

Selling costs for Property are higher than Shares. But as you can see below even with these extra selling costs, Property can still generate much higher returns than Shares, all due to the power of leverage.

NOTE: this example does not consider additional contributions (in Shares or onto the Mortgage), individual’s tax obligations or benefits, benefits of property depreciation, or the income generated by either option. These factors should be considered before you embark on any investment.

Risks and Rewards of Property Leverage

Leveraged property investing offers significant rewards but also comes with inherent risks. It's essential to weigh these carefully before diving in.

Rewards of leveraged Property:

- Higher potential returns on investment

- Ability to build a larger property portfolio

- Tax benefits and deductions

- Potential for passive income generation

Risks of leveraging:

- Increased vulnerability to market fluctuations

- Higher financial obligations (mortgage payments)

- Potential for negative cash flow if rental income doesn't cover expenses

- Risk of foreclosure if unable to meet loan obligations

Balancing these risks and rewards is crucial for successful leveraged property investing. Proper research, careful financial planning, and a solid understanding of the market are essential.

Strategic Property Investment Tips

Successful property investing requires more than just understanding leverage. This section will provide you with effective investment strategies, financial planning essentials, and tips for maximizing returns through leveraged investing.

Effective Investment Strategies

Developing a solid investment strategy is crucial for success in property investing. Here are some key approaches to consider:

- Value-add investing: Look for properties with potential for improvement. By renovating or upgrading, you can increase the property's value and rental income.

- Buy and hold: This long-term strategy involves purchasing properties and holding them for extended periods, benefiting from appreciation and rental income.

- Rent-vesting: If you can’t afford to buy your own home where you live, you can invest in a property in a more affordable market so that you get into the property market sooner and start to accumulate equity/wealth.

Remember, the best strategy depends on your current position in life, financial goals, risk tolerance, and market conditions. It's often beneficial to diversify your approach.

Financial Planning Essentials

Effective financial planning is the backbone of successful property investing. It involves careful budgeting, risk assessment, and long-term strategizing.

Start by clearly defining your investment goals. Are you aiming for passive income, long-term appreciation, or a mix of both? Your goals will shape your investment decisions.

Next, assess your financial situation. This includes evaluating your income, expenses, assets, and liabilities. Create a realistic budget that accounts for property-related costs such as mortgage payments, maintenance, and potential vacancies.

Finally, develop a risk management strategy. This might include maintaining an emergency fund (buffer) obtaining appropriate insurance coverage, and diversifying your investments to spread risk.

Maximizing Property Returns with Leverage

Leveraging property effectively can significantly boost your returns. Here are some tips to maximize the benefits of leverage:

- Choose properties with strong cash flow potential to ensure you can cover your mortgage payments and other expenses.

- Choose A-grade assets in quality locations, ones which will sell easily and quickly should you ever need to liquify your assets.

- Consider properties in areas with high growth potential to benefit from appreciation.

- Regularly review and refinance your loans to take advantage of better interest rates or terms.

It's crucial to maintain a balanced approach. While higher leverage can increase potential returns, it also increases risk. Aim for a leverage ratio that aligns with your risk tolerance and financial goals.

Remember, successful leveraged property investing requires ongoing education, market awareness, and adaptability. Stay informed about market trends, tax laws, and financing options to make the most of your investments.

DISCLAIMER: Niva Property Buyers or any of our representatives are not financial advisers and are not licensed to provide financial advice. The above information is also very generic in nature and is not aligned to any one individual’s circumstances. You should seek advice from your accountant and/or financial adviser on what is best for you. We believe strongly in diversification and believe that shares, property and other asset classes should form a part of an balanced portfolio. This article claims leverage is the main reason real estate is the best investment vehicle in Australia, however, you should always do your own research and consider your own situation.